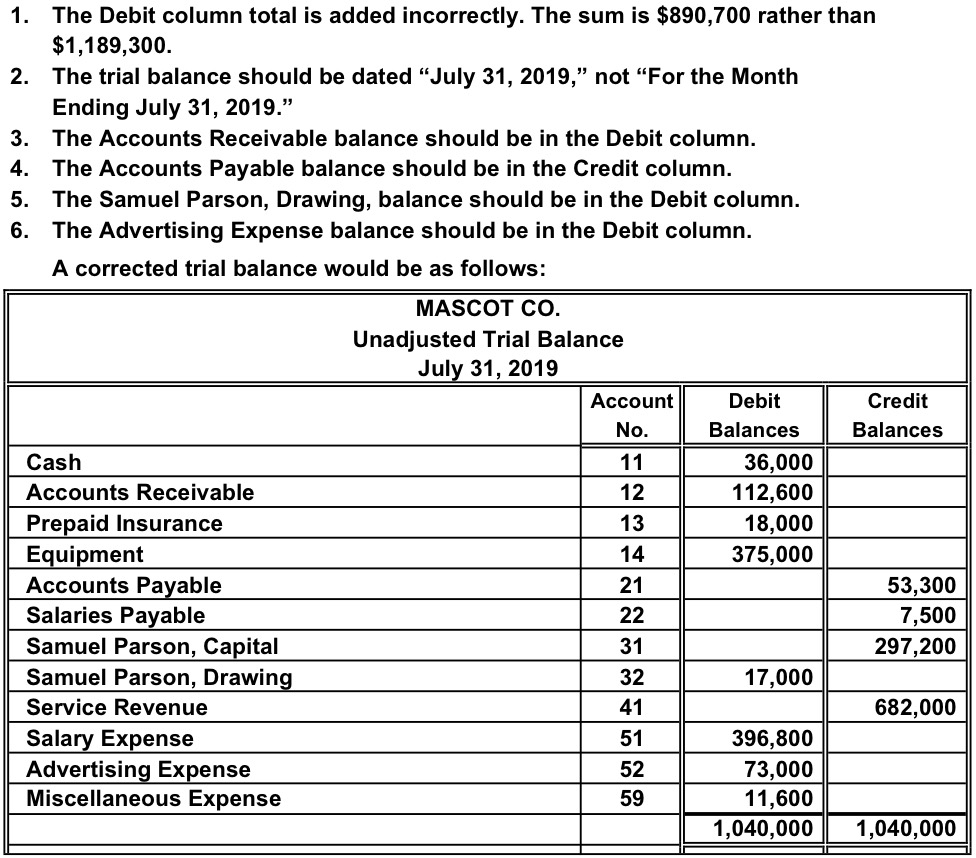

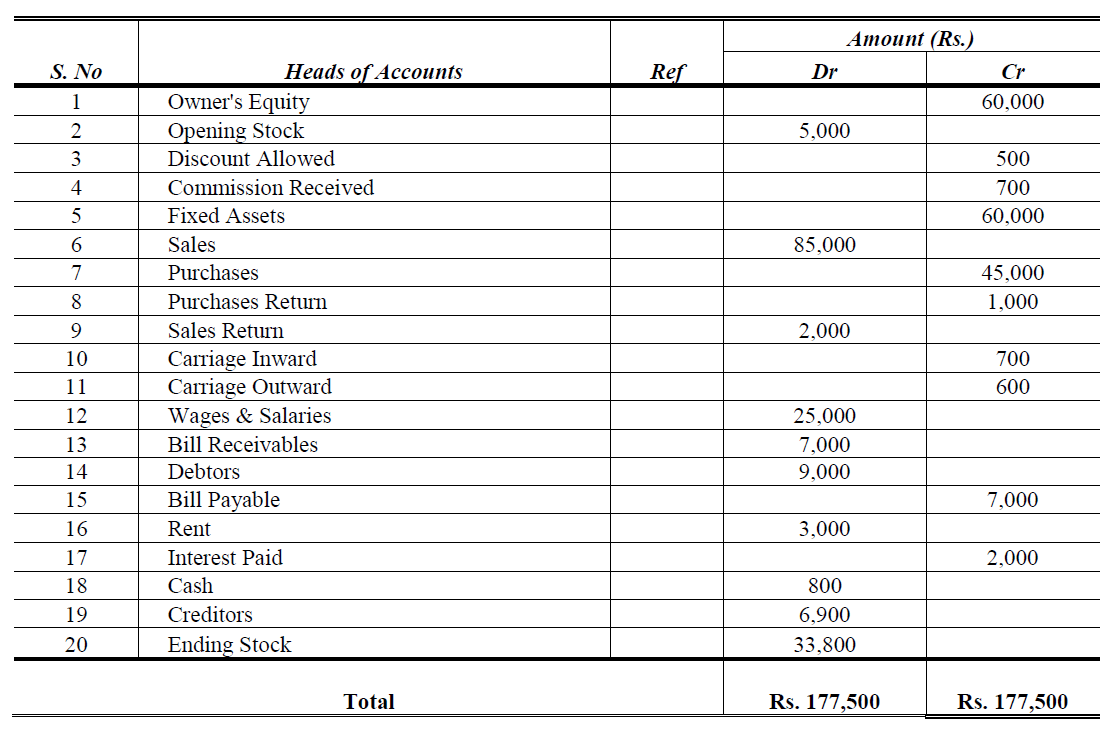

The Secret Of Info About Locating Errors In Trial Balance

Ppt Financial Accounting Powerpoint Presentation, Free Download Id

Trial Balance And Rectification Of Errors Teaching Resources

Errors Disclosed By The Trial Balance Youtube

Ppt Recording Business Transactions Powerpoint Presentation, Free

Trial Balance Meaning, Purpose, Sides, Sheet, Undetectable Errors, Etc

Ppt Accounting For A Service Business Unit 1.8 Powerpoint

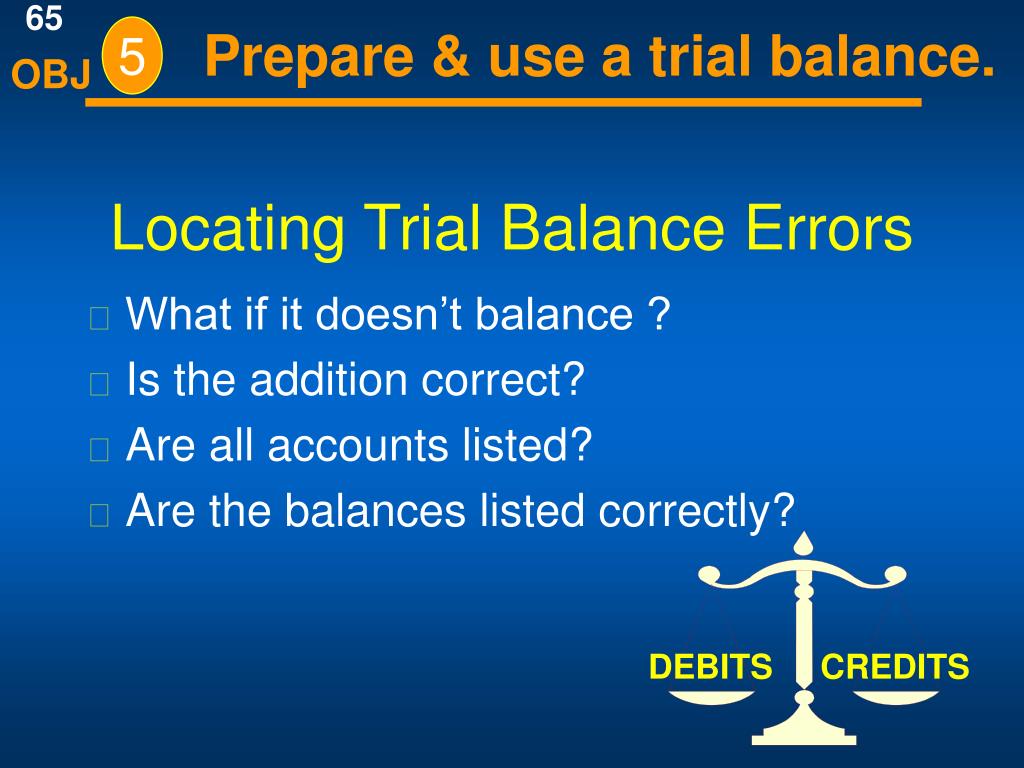

Procedure to locate errors in a trial balance.

Locating errors in trial balance. Steps to locate error in trial balance. Steps to locate errors in a trial balance. Steps to locate errors differences in the trial balance, howsoever minor they may be, must be located and rectified.

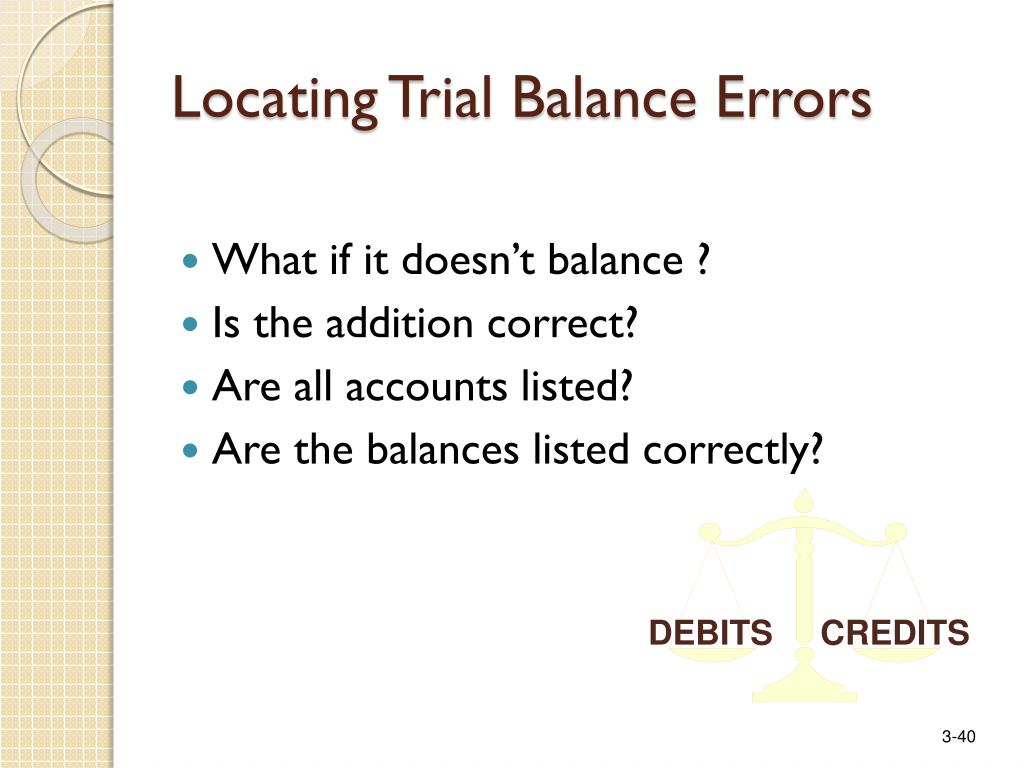

This means that there is an error in the trial balance or in the accounts. Check for any omission of account and recording that entry in trial balance. Following are the steps to locate the errors:

If you do find errors in your journal summaries, correct them, reenter the totals correctly, change the numbers on the trial balance worksheet to match your corrected totals, and retest your trial balance. The errors in a trial balance can be located by taking the following steps. Read this article to learn about the seven steps for detecting errors in trial balance.

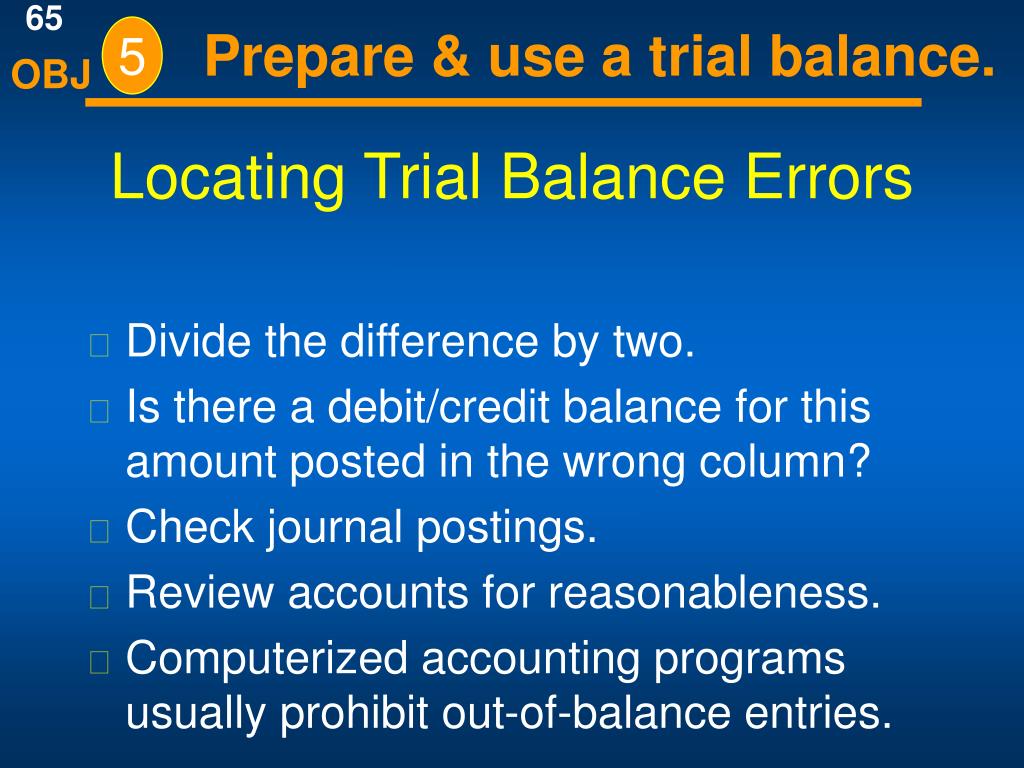

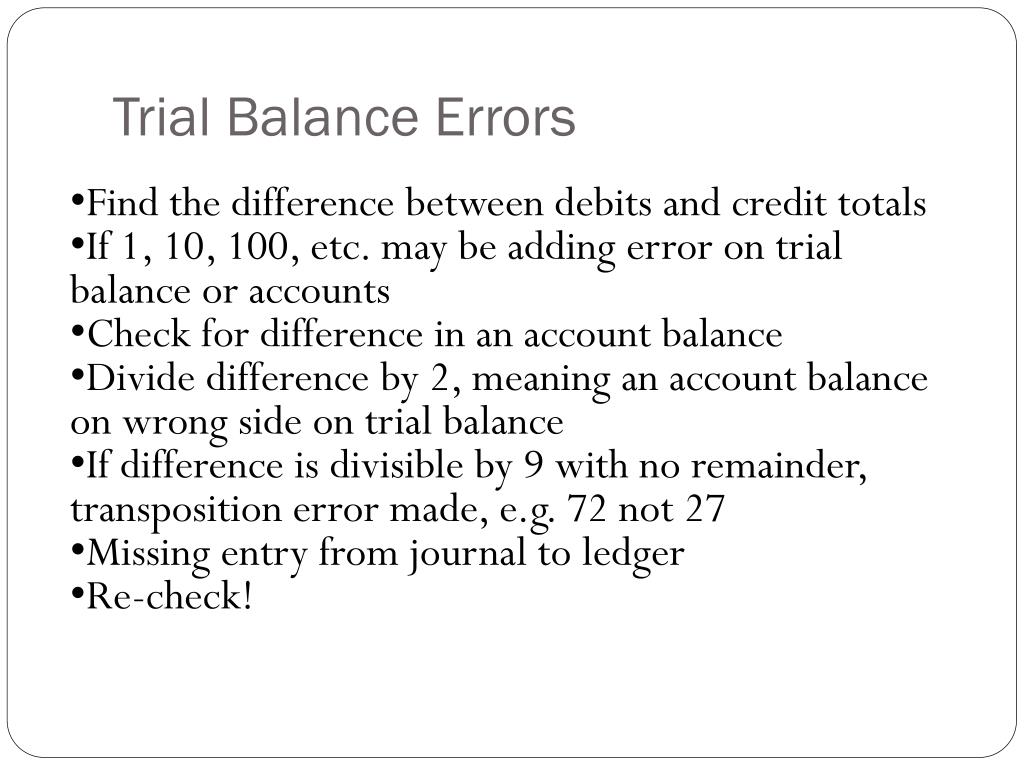

Verify the balance of each ledger account. For any lingering mistakes, use a suspense account. One way to find the error is to take the difference between the two totals and divide the difference by two.

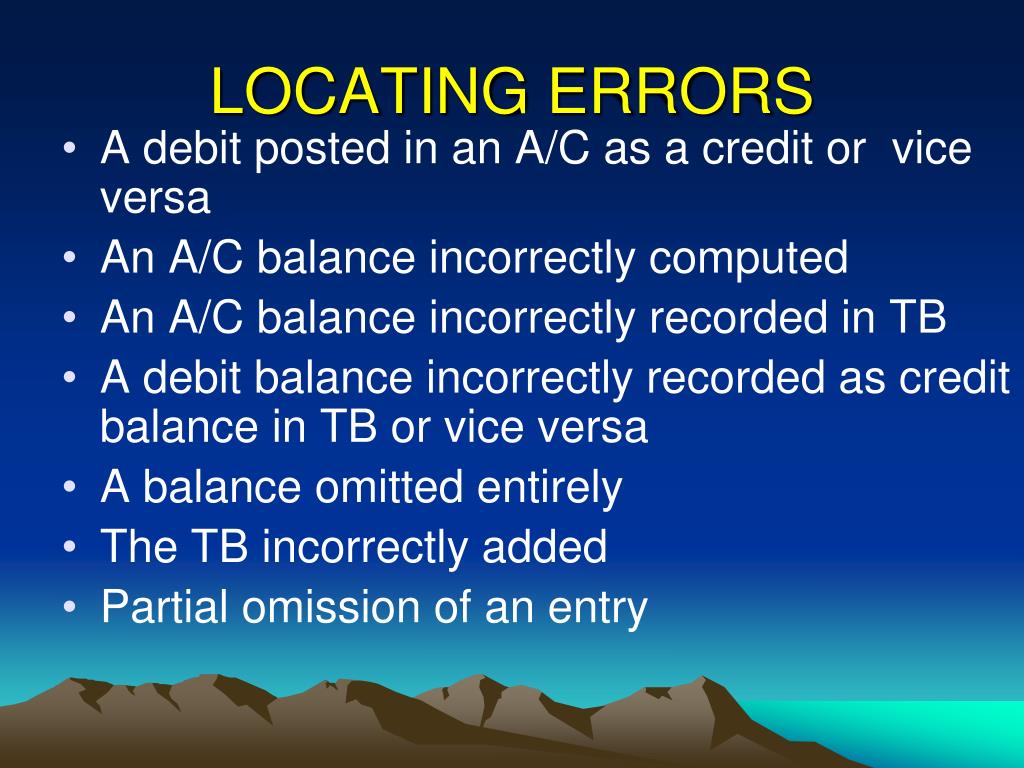

If the trial balance does not tally, the following procedure should carefully be followed: The final balance of an account is the difference between the total of the debit entries and the credit entries. Errors in trial balance are mistakes made during the accounting process that cannot always be detected by the trial balance.

Find out the amount of difference by the two columns, divided by 2 and see similar amount appears in the trial balance. 146 share 10k views 3 years ago acc 211 reviewing how to locate errors in a trial balance when your debits and credits don't equal. Check the total of debit and credit columns of the trial balance.

Trial balance is the third phase of the accounting cycle. Addition of both the columns ( debit and credit ) should be checked. Equate the account head in the trial balance with the ledger to check the difference in the amount or complete omission of the account.

The trial balance is a source of locating errors in a company's ledger. Compute the trial balance again. Calculate the exact difference in the trial balance.

These errors are classified under two heads: 2 types of limitations of trial balance are clerical errors, and errors of principles. Check that the cash balance and bank balance, discount allowed (if any) and discount received (if any) have been written in the trial balance correctly.

What steps do you perform to locate trial balance errors? Clerical errors are made by a human. Errors of principle happen when an accounting principle is not applied.

Errors Affecting Trial Balance Agreement Interactive Powerpoint

Accounting Questions And Answers Ex 220 Errors In Trial Balance

Rectification Of Errors Accountancy Knowledge

Detecting Trial Balance Errors Professor Victoria Chiu Youtube

Errors In Trial Balance Ppt Debits And Credits Corporations

Errors Disclosed By A Trial Balance Apk Upload

17+ Errors Affecting Trial Balance With Examples Pictures Petui

Errors That Affect The Trial Balance Accounting Resources For Students

Day 20 Locating The Errors Of Trial Balance Financial Accounting

Ppt Chapter 4.4 Trial Balance Powerpoint Presentation, Free Download

Ppt Recording Business Transactions Powerpoint Presentation, Free

Ppt Recording Business Transactions Powerpoint Presentation, Free

Trial Balance And Errors