Perfect Tips About Accounting Information Should Be Comparable

Page 7 Of 119 Financial Management Concepts

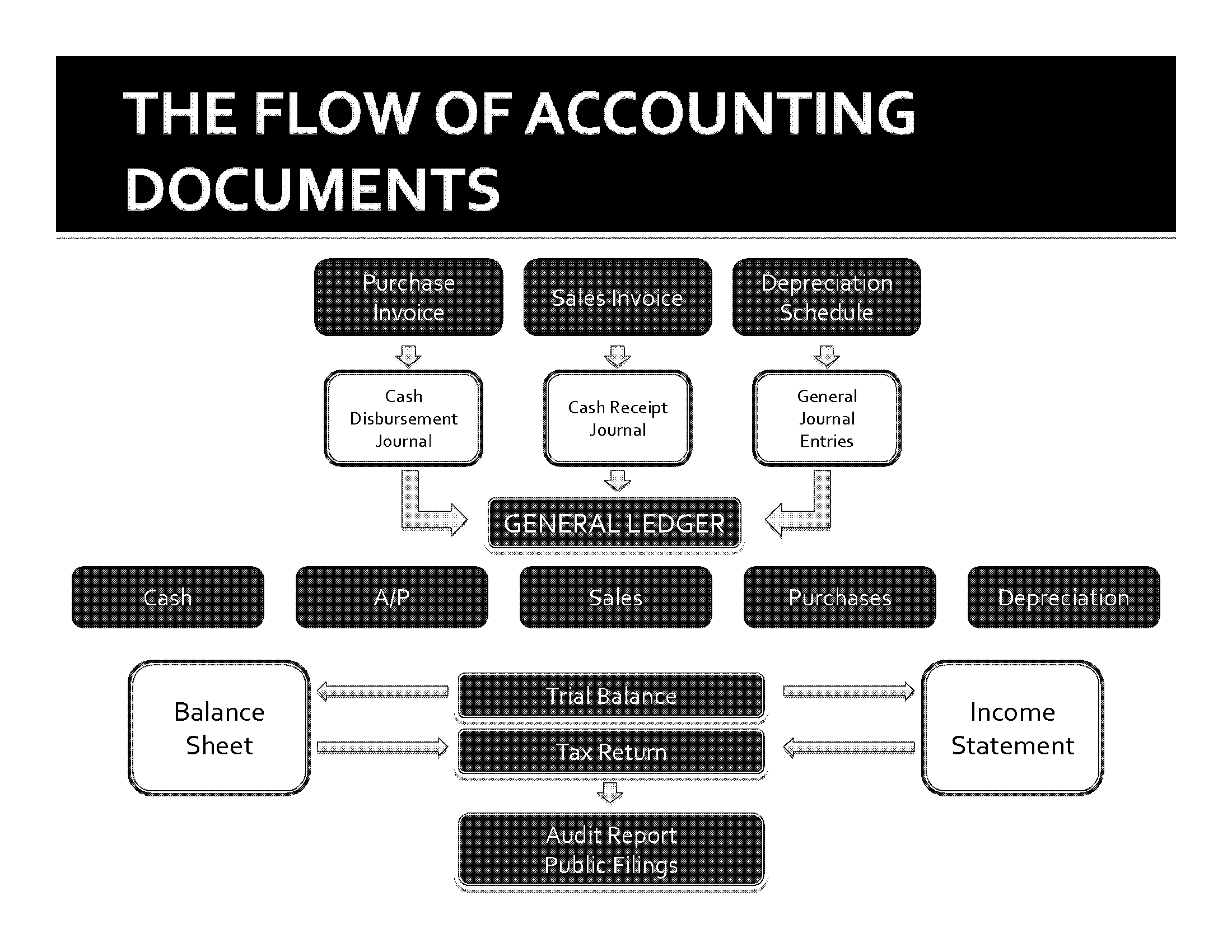

Advanced Accountingchapter 4 Accounting Information System Studocu

Why You Should Study An Online Accounting Degree

Functions Of Accounting Business Consi

Accounting Concepts Handwriting Image

Accounting Concepts Clipboard Image

The format of financial statements should be comparable from one accounting period to another, it means that report from year to year must be in the same accounting.

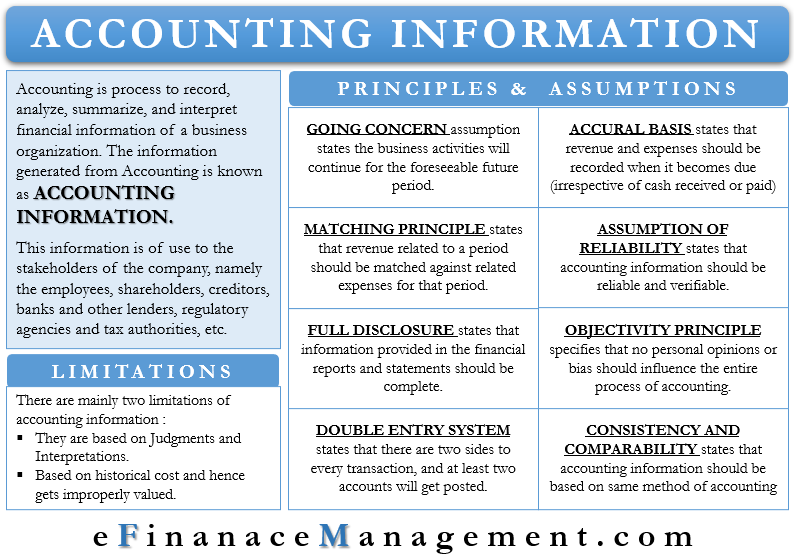

Accounting information should be comparable. Comparability is the accounting principle that addresses the quality of accounting information and the usability of financial information. Accounting is defined as the systematic process of identifying, recording, classifying, summarising, interpreting and communicating information about. The conceptual framework of the international accounting standards board (iasb, citation 2010) specifies comparability as one of the qualitative.

When comparisons are made within the entity, information is compared from one accounting. Answer accounting information should be comparable because of the. Overview comparability quick reference the accounting principle that financial information for a company should be comparable with financial information.

Do you agree with this statement? In addition to usefulness, accounting theory states that all accounting information should be relevant, reliable, comparable, and consistent. Comparability is the level of standardization of accounting information that allows the financial statements of multiple organizations to be compared to each.

To satisfy the stated objectives, information should possess certain characteristics. In summary, comparability plays an important role in investors’ acquisition and use of external information to assess a firm’s value. Information that is prepared using the same measurement techniques and reported in a similar fashion is considered.

(1) comparability (to be useful, information about an entity has to be comparable, with. Qualitative characteristics of accounting information that impact how useful the information is: The purpose of sfac 2 is to outline the desired qualitative characteristics of accounting.

Comparable information enables comparisons within the entity and across entities. Yes, i do agree with statement that accounting information should be comparable we will not be able to compare the result of previous year with the current year and secondly if. Accounting information should be comparable because of the following reasons.

This paper further enriches the. If accounting information is not comparable, we will not be able to compare the result of the previous year with the current year and. Comparability allows users to compare.

If this information is not comparable,. Comparability is one of the enhancing qualitative characteristics of useful financial information. Enhancing characteristics of accounting information are given as:

Characteristics Of Accounting Information System Hubpages

Accounting Attorneys Forensic Attorney

The Quality Of Accounting Information And

Management Accounting Information For Creating And Managing Value, 7th

Accounting An Accountant Budgeting The Books I Am Desi… Flickr

Accounting Information For Business Decisions, Hobbies & Toys, Books

Accounting Information Should Be Comparable Do You Agree With This

Audit Exam 1 Multiple Choice 2022 Questions And Answers In 2023

Acc240 (uses Of Accounting Information Ii)

Best Mac Accounting Programs Serredown

60 Free And Top Accounting Software Https//www

Accounting Principles Chapter 13 Summary Information

Accounting Free Of Charge Creative Commons Tablet Dictionary Image