Matchless Info About Ias 16 Standard

Ias 36 Overview Of The Standard Grant Thornton Singapore

Ias 16 Property Plant Equipment Depreciation International

(pdf) The Impact Ofthe Accounting And Financial System (scf)

Ias 16 Pdf International Financial Reporting Standards Depreciation

Ias 16 & 38 Intangible Asset International Financial Reporting

Ias 16 Property Plant And Equipment Full Standard Raelst

The european financial reporting advisory group (efrag) has launched the second part of its survey.

Ias 16 standard. Proceeds before intended use (amendments to ias 16) which prohibit a company from deducting from the cost of. Ifrs accounting standards are, in effect, a global accounting language—companies in more than 140 jurisdictions are required to use them when reporting on their financial. 45 rows international accounting standards (iass) were issued by the antecedent international accounting standards council (iasc), and endorsed and.

Efrag survey on ifrs 16 — user perspective. Valuation at depreciated replacement cost is. Ifrs accounting standards are developed by the international accounting standards board (iasb).

International accounting standard ias 16 property, plant and equipment january 2012 (incorporating amendments from ifrss issued up to 31 december 2011, including those. However, there are difficulties of obtaining a market value for plant and equipment that are recognised in ias 16. Ias 16 property, plant and equipment the objective of this standard is to prescribe the accounting treatment for property, plant and equipment so that users of the financial.

International accounting standard 16 property, plant and equipment or ias 16 is an international financial reporting standard adopted by the international accounting standards board (iasb). In may 2020, the board issued property, plant and equipment: The cost of property, plant and equipment (also known as ‘pp&e’) is composed of the following elements according to ias 16.16:

Ias 16 4 © ifrs foundation with ias 2 or ias 16 are recognised and measured in accordance with ias 37 provisions, contingent liabilities and contingent assets. Ias 16 property, plant and equipment sets out the requirements for the recognition of the assets, the determination of their carrying amounts, and the depreciation charges and. The standard provides a single lessee accounting model,.

It concerns accounting for property, plant and equipment (known more generally as fixed assets), including recognition, determination of their carrying amounts, and the depreciation charges and impairment losses The board clarified that the requirements of ias 16 apply to items of property, plant and equipment that an entity uses to develop or maintain (a) biological assets and (b) mineral. Ias 16 property, plant and equipment was issued by the international accounting standards committee in december 1993.

Overview ifrs 16 specifies how an ifrs reporter will recognise, measure, present and disclose leases.

Ias 16 July 2011 Property, Plant And Equipment (july

Ias 16 Property, Plant And Equipment Summary Youtube

Ias 16 Property, Plant And Equipment Gcs Malta

Ias 16 Property, Plant And Equipment

Ias 16 Standard On A Page (soap) Youtube

Ias 16

Ias Officer With Varied Experience Ravneet Kaur, First Woman Chief Of Cci

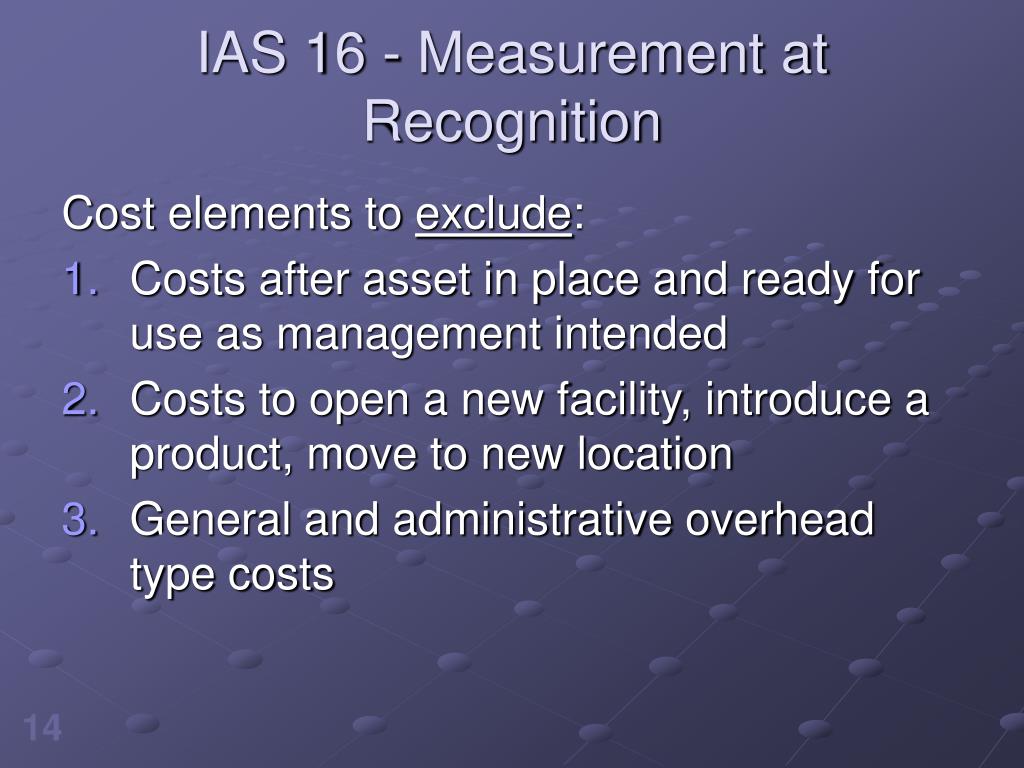

Ppt Property, Plant And Equipment Ias 16 Powerpoint Presentation

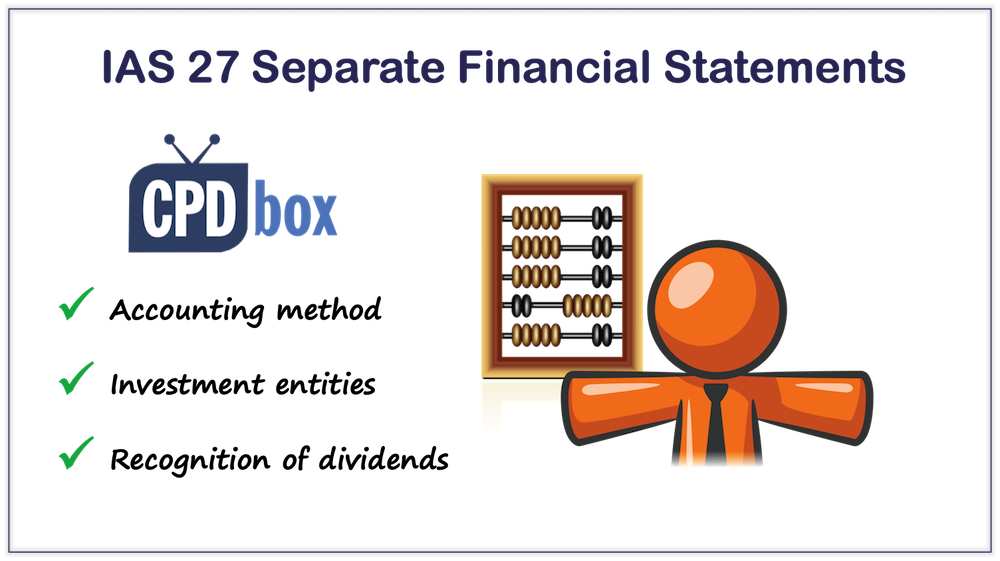

Ias 27 Separate Financial Statements Cpdbox Making Ifrs Easy

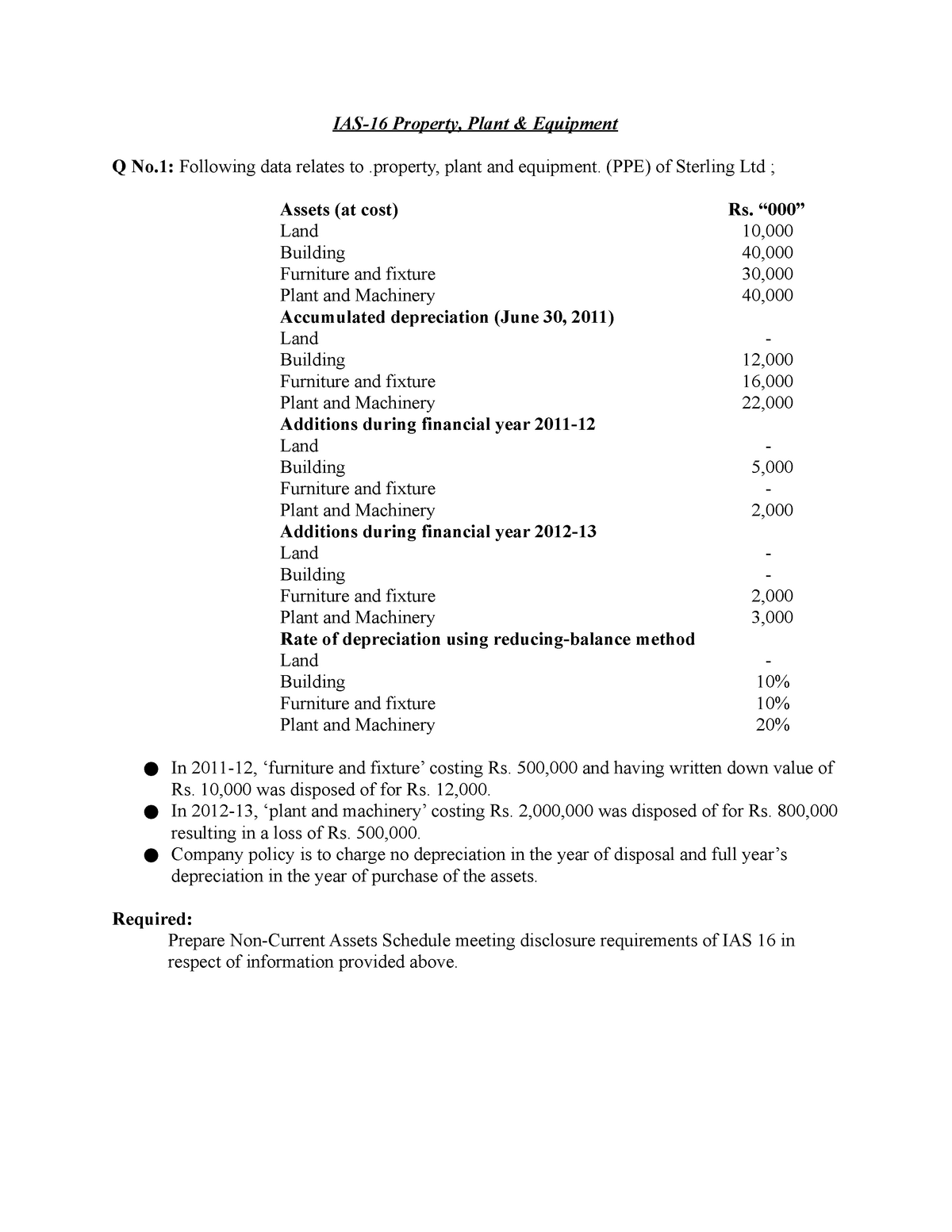

Ias16fall 2020updated Ias16 Property, Plant & Equipment Q No

Ias 16.pdf

Ias 16 Standard Property, Plant And Equipment In April 2001