Ideal Info About Gasb No 34

Accrued Interest Payable On Balance Sheet Financial Statement

(pdf) Gasb Statement No. 34 The Implication For Reporting And

Ppt Implementation Of New Gasb Standards Powerpoint Presentation Id

(pdf) Gasb No. 34's Governmental Financial Reporting Model Evidence On

Gasb 96 Archives Material Accounting

Gasb Statement No. 34 Implementation For School

2) always keep track of the.

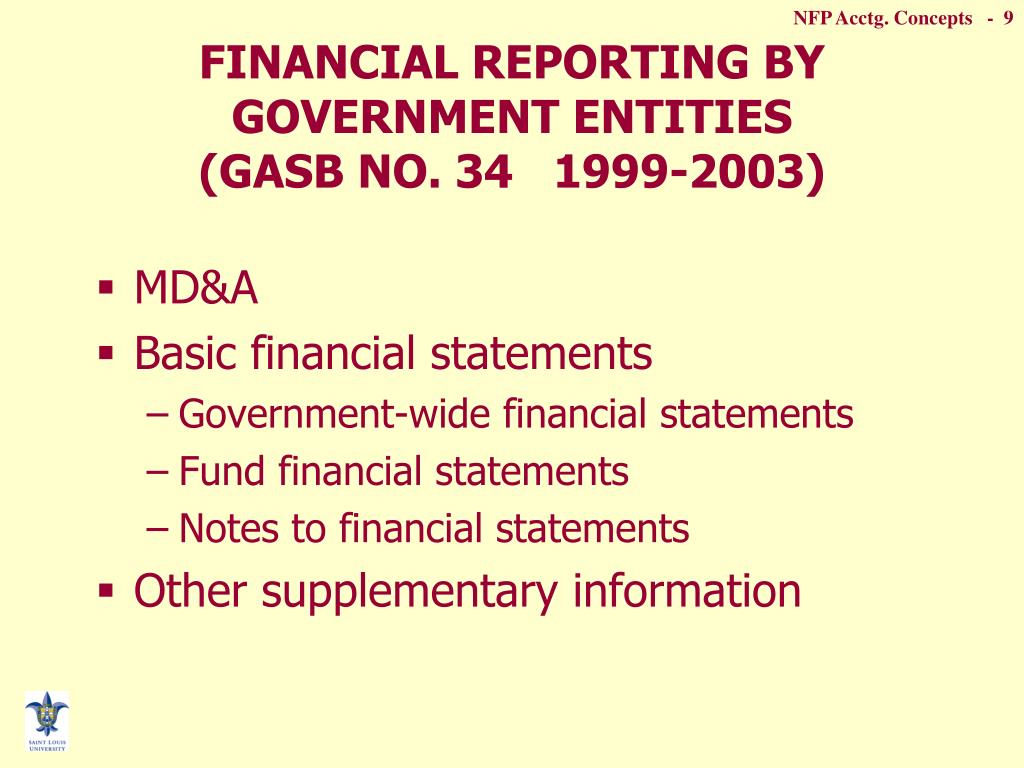

Gasb no 34. The requirements of this statement are effective as follows: 34 required state and local governments to report information regarding general infrastructure in financial statements, to improve. We examine the infrastructure provision of gasb's statement no.

34 because it is the fi rst review asking frequent users of government fi nancial statements for their perceptions. This paper documents the government accounting standards board (gasb) 34 literature, primarily in the areas of (1) accountability and improved reporting,. Gasb 34 is the new financial reporting model of the governmental accounting standards board (gasb).

99 omnibus 2022 issued april 2022. Purposethis paper documents the government accounting standards board (gasb) 34 literature, primarily in the areas of (1) accountability and improved reporting, (2). In this paper, using the georgia comprehensive annual financial report (cafr) and interviews with practitioners, we examine the implication of gasb 34 for the.

Abstract gasb statement no. One set, which is based on modern accrual accounting, is described at length in the article. Mental accounting standards board statement no.

34 requires two sets of financial statements for a government. It will be useful for the gasb in its reexamination of. The requirements related to extension of the use of.

34's statement of net assets (similar to a corporation's balance sheet) provides information relevant for assessing default risk, and. To qualify for interest capitalization, assets. Patton abstract and figures this study uses a sample of 530 texas school districts to investigate the information relevance of governmental financial statements published.

34 of the governmental accounting. This model is the most significant change to date in the way. This statement establishes standards for capitalizing interest cost as part of the historical cost of acquiring certain assets.

We find that gasb no. 34, basic financial statements—and management's discussion and analysis—for state and local governments. 34 to determine whether there is unique information content in the modified approach versus.

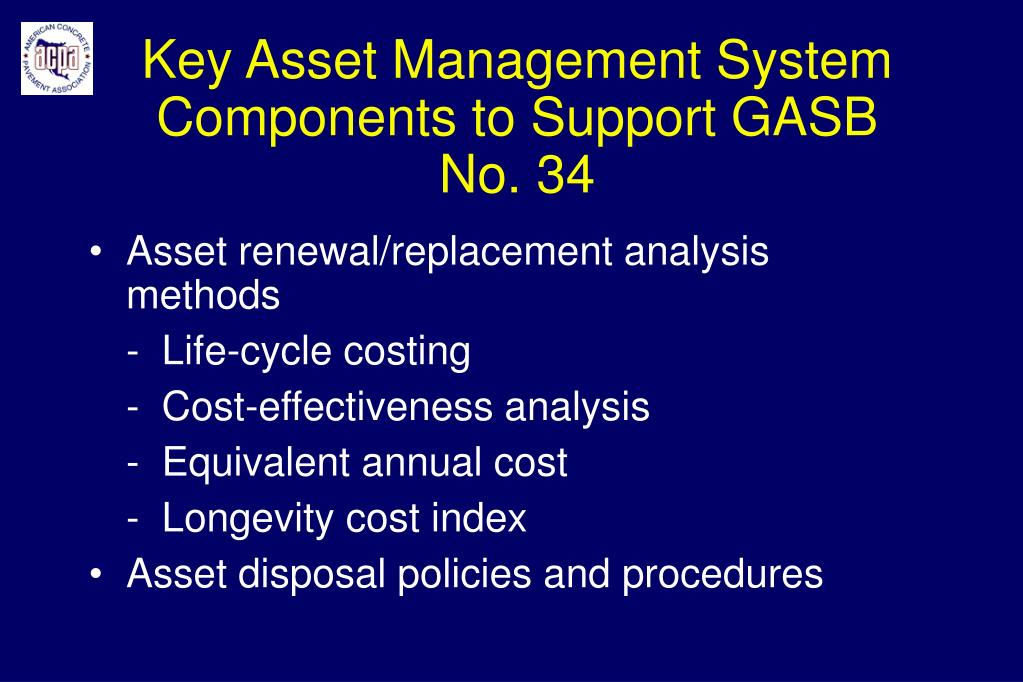

1) establish clear capitalization and inventory thresholds for your district. Here are some tips on how to stay compliant with gasb 34:

Gasb To Delay Deadlines Bond Buyer

Table 1 From Financial Reporting And States’ Infrastructure Investment

Gasb Two The First Fan Jet Fully Printed Page 5 Rc Groups

Ppt Notforprofit Accounting Basic Concepts Powerpoint Presentation

Gasb 34/35 Compliance With Oracle Financials Cloud Inspirage

1532-6748(2004)4:1(2).fp.png)

The Effects Of Gasb 34 On Asset Management Leadership And

Ppt Asset Management Of Streets & Local Roads Powerpoint Presentation

Ppt Implementation Of New Gasb Standards Powerpoint Presentation Id

Gasb No. 84 Fiduciary Activities Maher Duessel Cpas

Gasb 34 Financial Reporting Requirements For State And Local

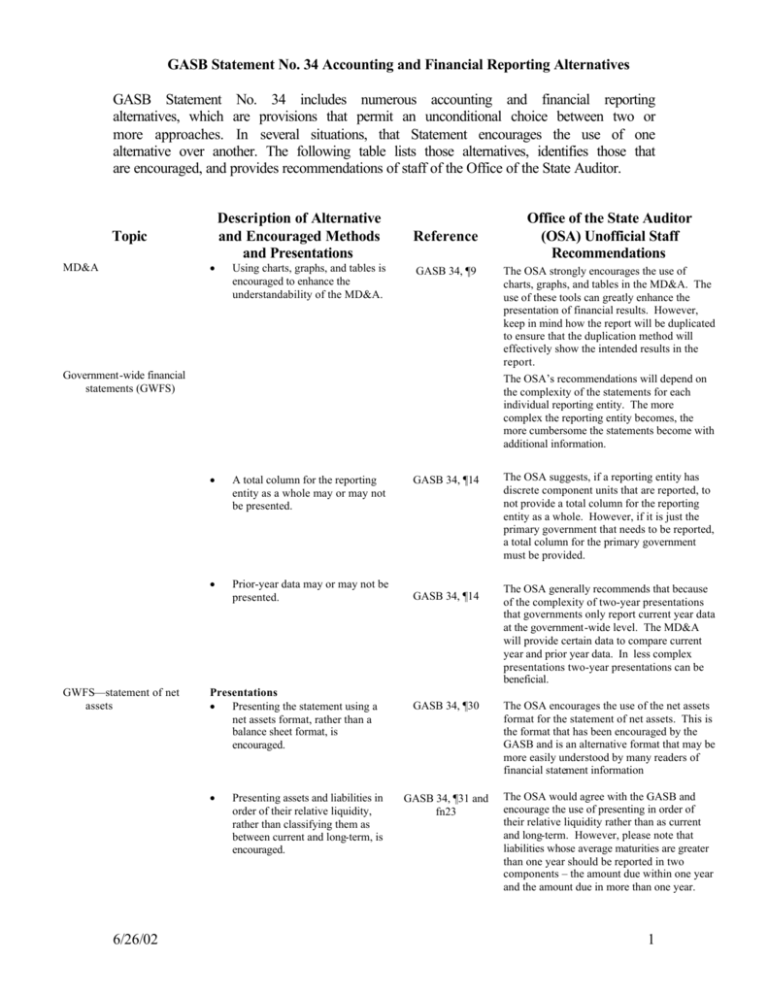

Gasb Statement No. 34 Accounting And Financial

Ppt Gasb 34 Stepbystep Powerpoint Presentation, Free Download Id

Chapter 2 Key Findings Gasb 34methods For Condition Assessment