Peerless Info About Sme Financial Statements

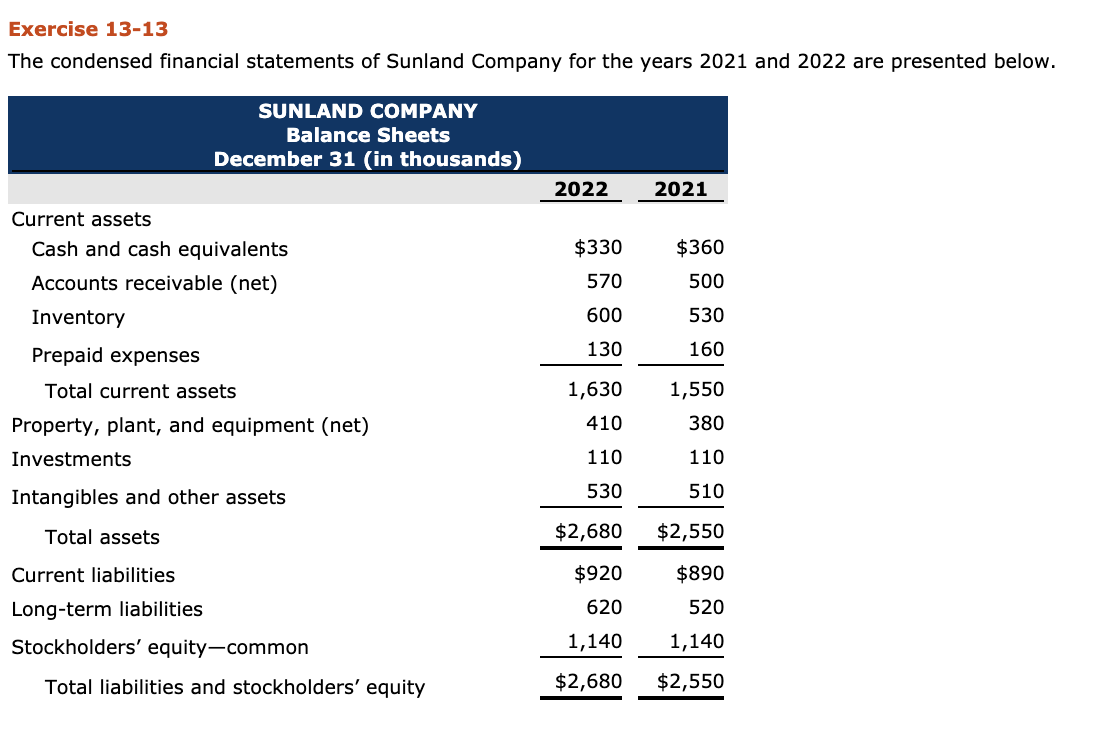

Solved Exercise 1313 The Condensed Financial Statements Of

Activity For Sme International Financial Reporting Standards

Sme Financial Statements

Financial Statements Cfo 2013 Annual Report

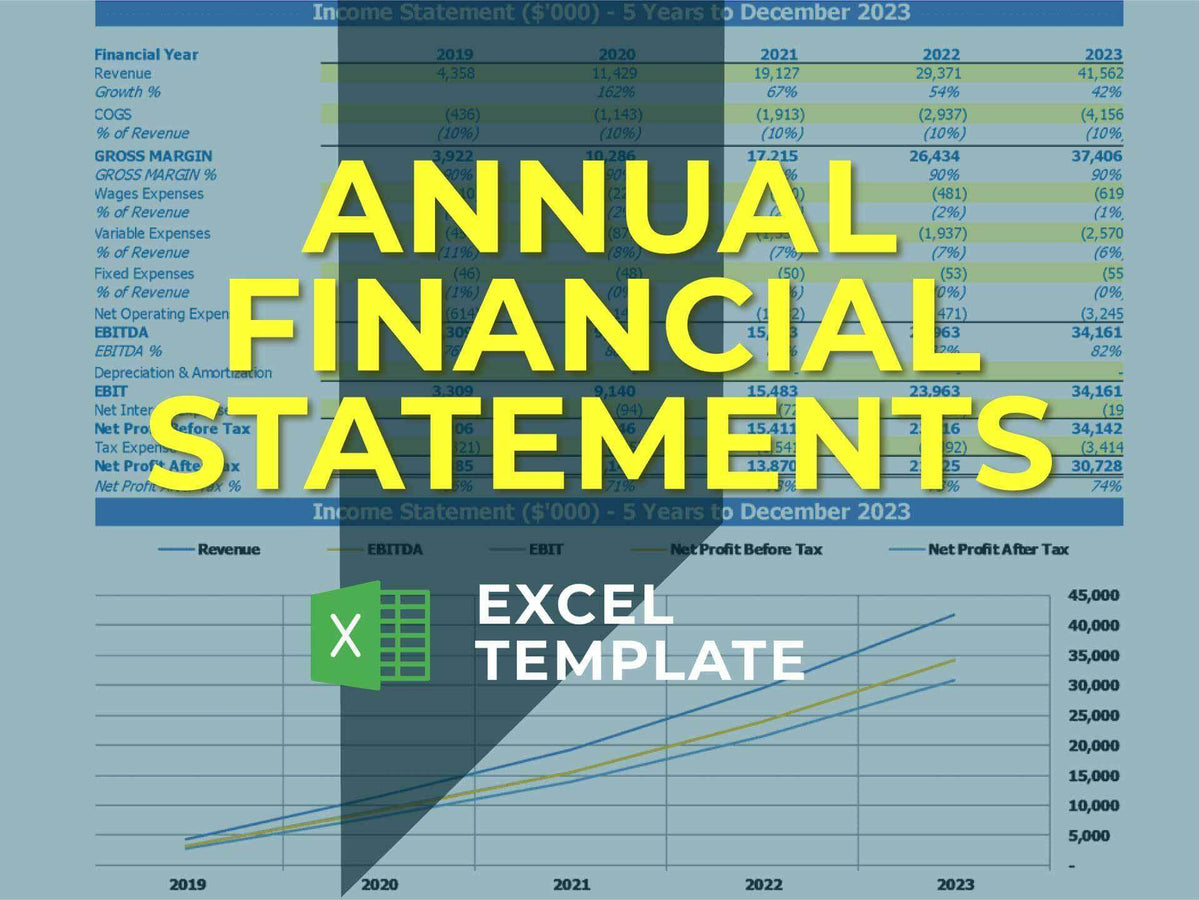

8 Free Financial Statement Templates Word Excel Sheet Pdf

4 Ways Inventory Management Affects Sme Financial Statements

Accounting framework of the ifrs for smes 2.

Sme financial statements. Track all revenue, payments, deposits, invoices and business expense records because you will need that information to create financial statements. The accounting policies disclosed in the illustrative financial statements reflect the facts and circumstances of the fictitious entity on which these financial statements are. Consolidated financial statements.

Gaap the frf for smes is the tool to prepare streamlined, relevant financial statements for. The financial statements are presented in. The needs of lenders, creditors and other users of smes’ financial statements who are primarily interested in information about cash flows, liquidity and solvency;

Section 3 sme financial statement presentation scope of this section fair presentation compliance with the ifrs for smes going concern frequency of reporting consistency. This module focuses on the presentation of the notes to financial statements applying section 8 notes to the financial statements of the ifrs for smes standard. Purpose financial statements for external users.

Ifrs for smes illustrative financial statements for close corporations (included from page 84 to138 of the saica close corporations guide) The financial statements are presented in. Section 9 consolidated and separate financial statements of the ifrs for smesstandard issued by the international accounting standards board in october 2015 with extensive.

Summary of the ifrs for smes special edition of deloitte's ias plus newsletter on the ifrs for smes click to download a special edition of our ias plus. Presentation of income under ifrs. Example reflects full set of illustrative financial statements with the notes block as well as detail tagged.

Business’s financial statements based on the needs of bankers and other users. The ifrs for smes on which the illustrative financial statements have been prepared was issued in may 2015 and becomes effective for periods beginning on or after 1 january. Section 9 of the standard sets out when and how an sme prepares consolidated financial statements.

The financial statements cover rsm sme(3.23)(b),(d), ifrs for sme limited as an individual entity.

Small Business Statement Templates Smartsheet

Sample Reporting Documents For A Company/group Applying Smefrs The

Sme Financial Statements Solution Caseware Africa

(pdf) A Comparative Evaluation Of South African Sme Financial

Sme Financial Statement Small And Medium Sized Enterprises

Ifrs For Sme27s Financial Statements Template Expense Depreciation

(pdf) Microsme Characterization From Financial Statements

01 Illustrative Examples Financial Statements For

13+ Different Types Of Financial Reports En 2020

Ifrs Illustrative Consolidated Financial Statements For Smes 2017 By

The Ifrs For Smes

Financial Statement Format Get Free Excel Template

Portrait Of Sme Business Owner, Woman Using Computer And Financial