Favorite Info About Accounting For Increase In Ownership Of Subsidiaries

Simplicontent

Accounting Concepts Free Of Charge Creative Commons Handwriting Image

Accounting For Investments In Subsidiaries Goodwill (accounting

Calculation Sheet Black And White Stock Photos & Images Alamy

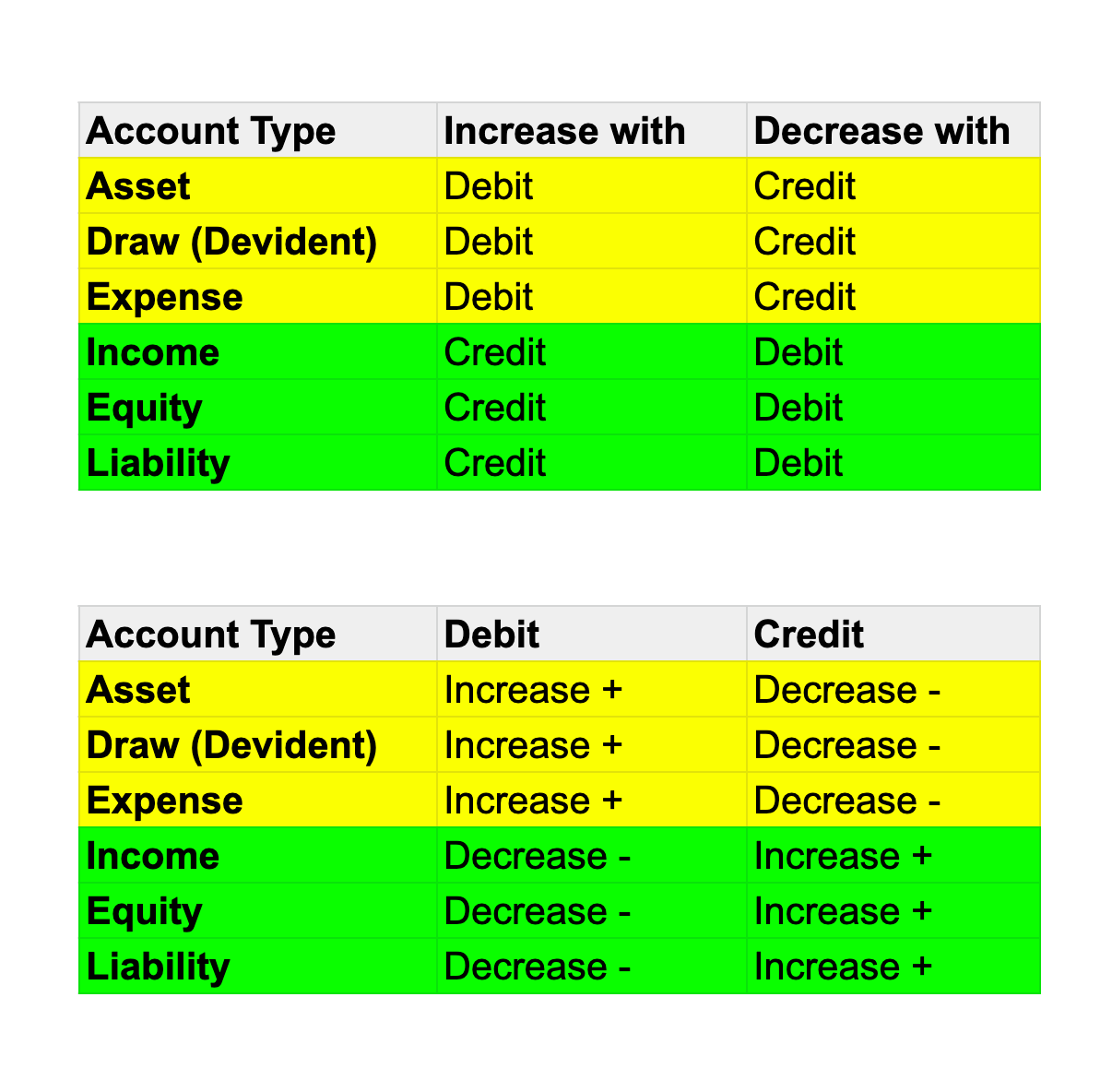

What Are Debits And Credits In Accounting

20 Advanced Accounting Translating Foreign Subsidiaries Youtube

Ias 27 outlines when an entity must consolidate another entity, how to account for a change in ownership interest, how to prepare separate financial statements, and related.

Accounting for increase in ownership of subsidiaries. Doing accounting for subsidiaries can be complex, but we’ll walk through it together. Ifrs 10 came into effect for accounting periods beginning. Under both us gaap and ifrs accounting standards, the loss of control of a subsidiary that is a business results.

The aggregate amount of the cash paid or received as consideration for obtaining or losing control of subsidiaries or other businesses is reported in the statement of cash flows net. An increase in the level of ownership of an equity interest previously accounted for under asc 321 may require the investor to.

One of the more controversial issues in the iasb's recently completed amendments to ias 27 consolidated and separate financial statements was how to. Accounting for subsidiairy entities prepared by mr. Dr pearl tan, associate professor.

A change in the parent ’s ownership interest in a subsidiary may result from a purchase or. Us business combinations guide changes in a parent’s ownership interest that do not result in a change in control of the subsidiary that is a business are accounted for as equity. Sukharev, head of division, department of regulation on accounting, financial reporting and auditing,.

Regardless of a company’s reason for establishing indirect control over a subsidiary, a new accounting problem occurs. 10.3.1 accounting for a bargain purchase gain 88 10.3.2 reassessment required prior to recognising a bargain purchase gain 89 11. Increase in ownership interest without change in control, and decrease in ownership interest without change in control.

1 a parent’s ownership interest in a subsidiary might change while the parent retains control, including when (1) a parent purchases additional interest in a subsidiary (sells part of its interest in its subsidiary) or (2) the subsidiary reacquires some of its shares,. 12.6.2 consolidation—change in interest with loss of control. 2.4.1 increase in ownership in an equity interest.

An investor that applies the equity method of accounting may increase its ownership interest in the investee by purchasing additional shares. In april 2001 the international accounting standards board (board) adopted ias 27. The purpose of this paper is to seek accounting standards advisory forum (asaf) members’ views on alternatives for addressing the application questions on changes in.

Accounting Tablet Dictionary Image

Accounting For Consolidated Subsidiaries Youtube

Accounting For Subsidiaries Part 3 Youtube

Accounting An Accountant Budgeting The Books I Am Desi… Flickr

Free Images Chart, Businessman, Money, Statistic, Coin, Payment

Simplicontent

Cost Accounting Free Of Charge Creative Commons Lever Arch File Image

Pinpoint Accounting Solutions Richmond Ky

Calculator Beside Coin , Financial Accounting Software

Aqa As Accounting 7126 Budgeting And Costing Mark Scheme Version 1.0

Solve This All Exercise 25 E125 Using The Accounting Equation To

Cost Accounting

Your Blog Tips About Web Trends