Best Of The Best Tips About Goodwill Impairment Loss Journal Entry

Goodwill Impairment Testing Navigate Economic Volatility Crowe Llp

Goodwill Impairment Test Example Of

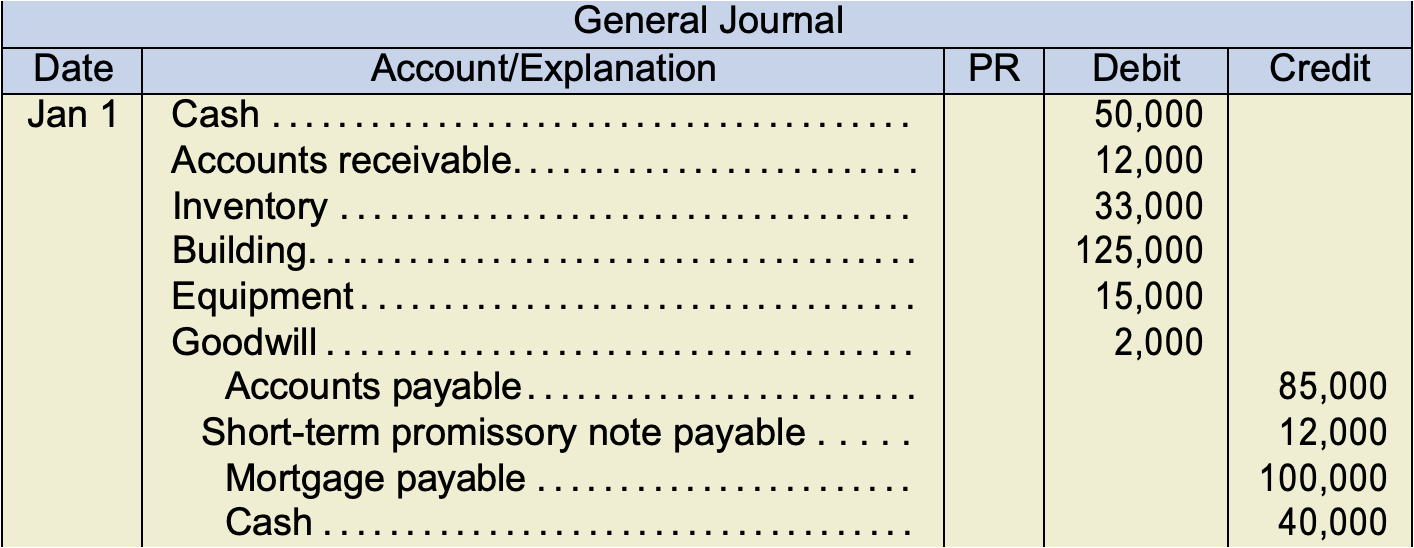

Self Study Notes Accounting For Asset Exchanges

Ppt Consolidated Statements Subsequent To Acquisition Fundamentals

Reversal Of Impairment Loss For Goodwill In Corporate Accounting

Goodwill Impairment Definition, Examples, Standards, And, 46 Off

Accounting for reversal of an impairment.

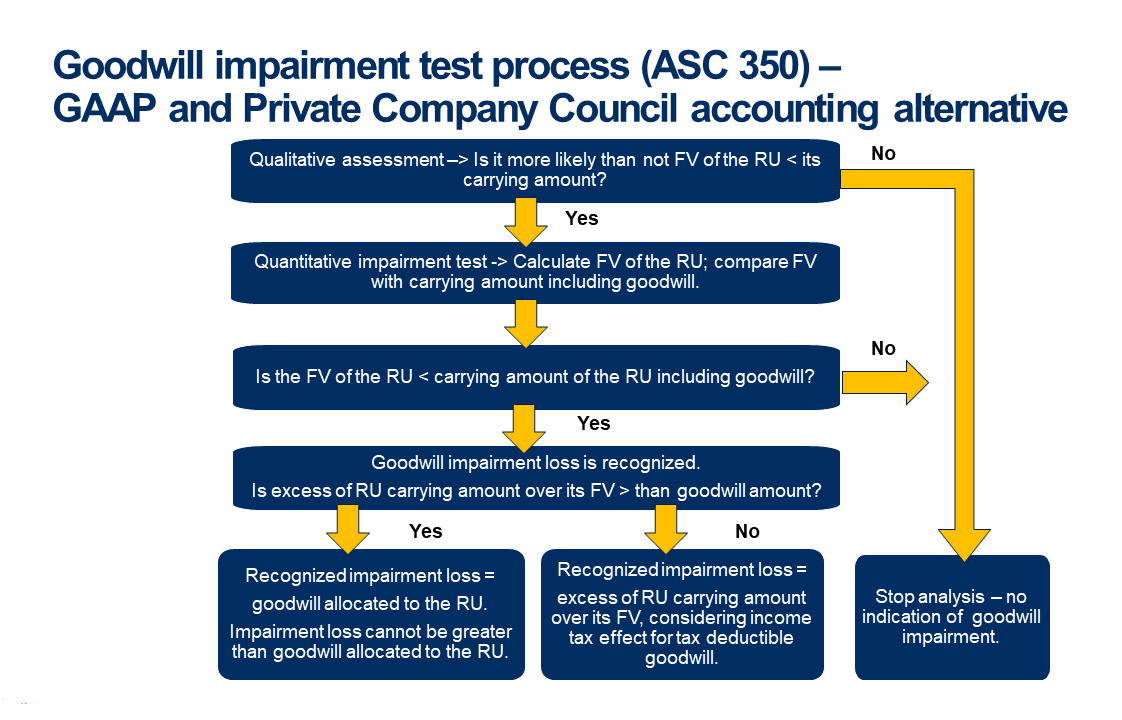

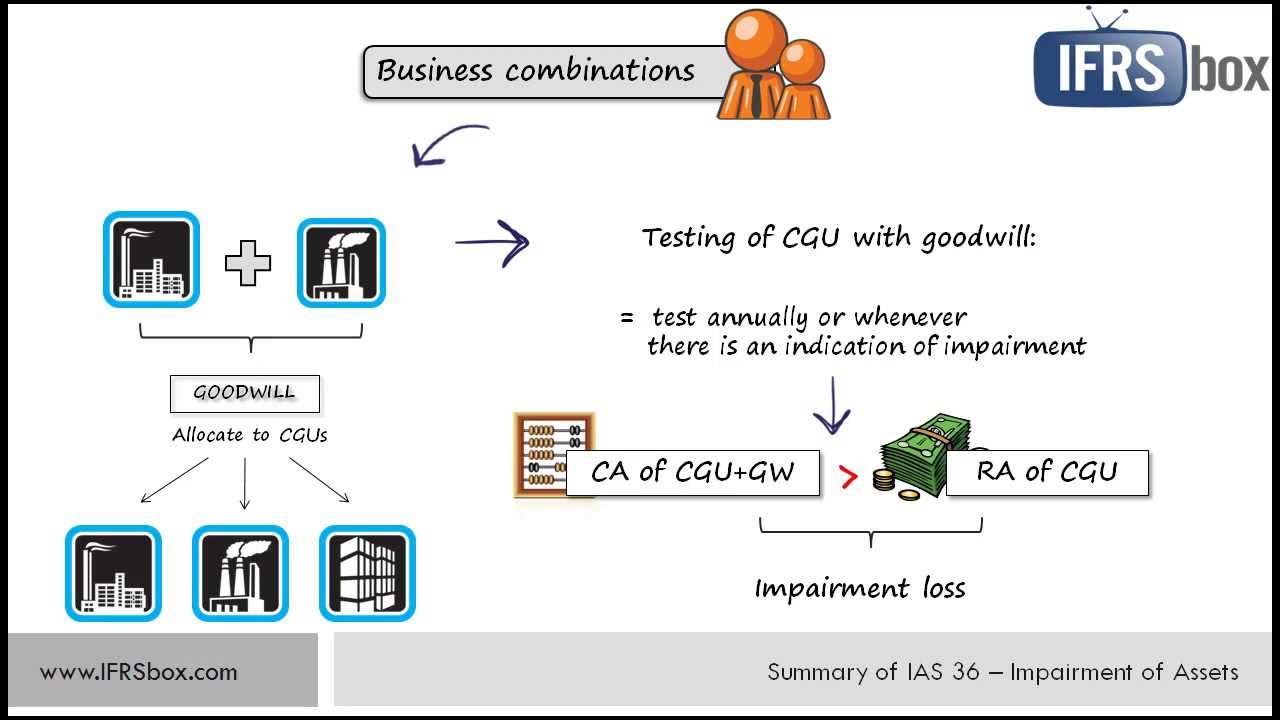

Goodwill impairment loss journal entry. An impairment loss is recognised immediately in profit or loss (or in comprehensive income if it is a revaluation decrease under ias 16 or ias 38). The impairment loss will be applied to write down the goodwill, so that the intangible asset of goodwill that will appear on the group statement of financial position will be $270. The impairment loss will be applied to write down the goodwill, so that the.

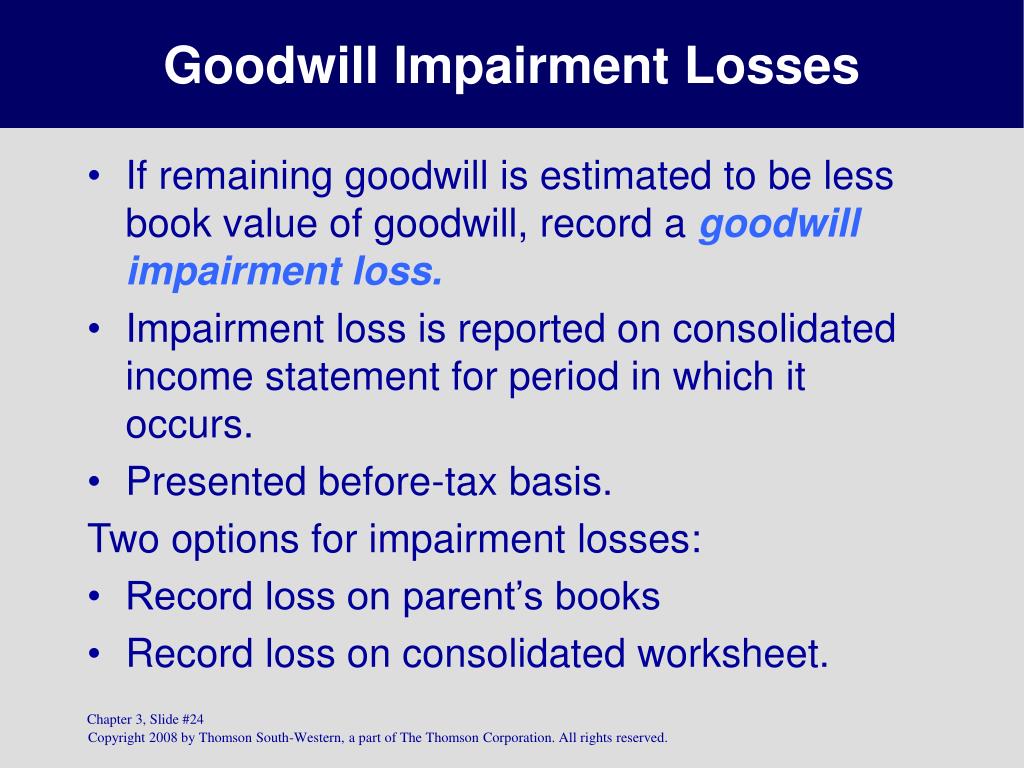

Record the journal entry to recognize any goodwill impairment. Any excess of the carrying value over the implied fair value is recognized as an impairment loss. The company can make the journal entry for goodwill impairment by debiting the goodwill impairment account and crediting the goodwill account when it finds out that there is an impairment of goodwill as a result of periodic review.

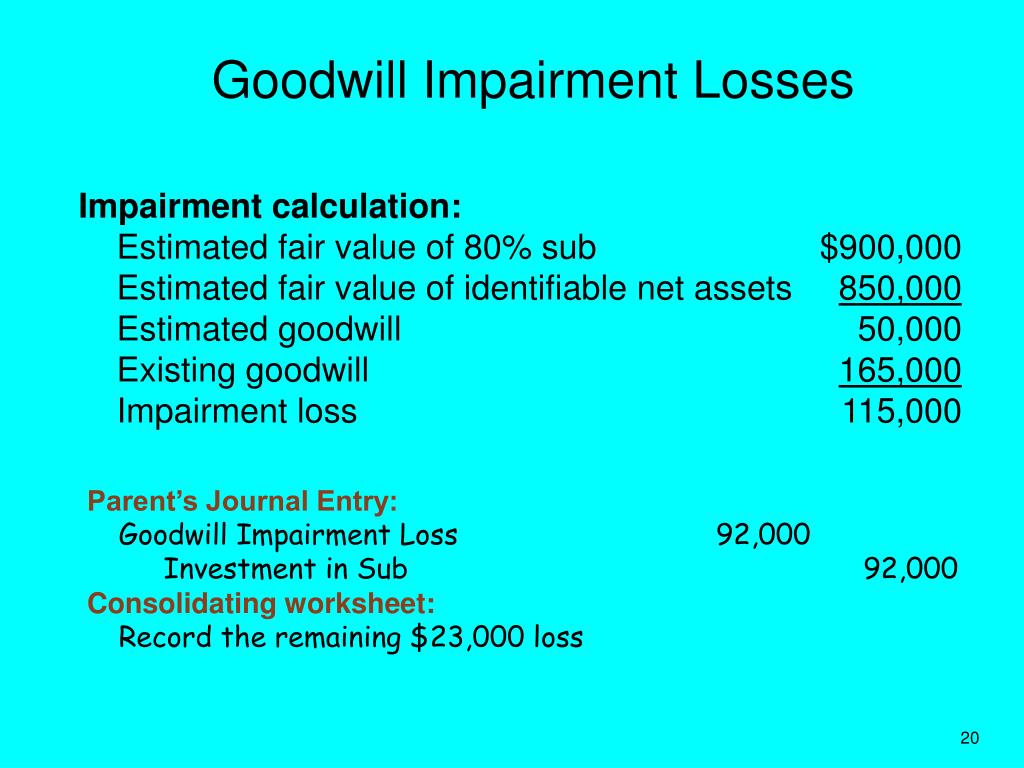

Only the parent’s share of the goodwill impairment loss will actually be recorded, ie 60% x $50 = $30. Any goodwill impairment loss is recognized for both the parent and nci, and allocated between both on a rational basis. If the goodwill account needs to be impaired, an entry is needed in the general journal.

Goodwill impairment is a charge that companies record when goodwill's carrying value on financial statements exceeds its fair value. Journal entries for impairment testing transactions. Goodwill impairment accounting occurs when the carrying value of goodwill on financial statements exceeds its fair value, leading to the declaration of a goodwill impairment.

Journal entry find out impairment loss if any given the following data for two reporting units: To illustrate the concept of. Goodwill impairment is an expense item on the income statement.

(pdf) Goodwill Impairment

Asu 201704 Intangiblesgoodwill And Other; Simplifying The Test For

11.3 Goodwill Intermediate Financial Accounting 1

Ppt Consolidated Statements Subsequent To Acquisition Chapter 3

(pdf) Determinants Of Goodwill Impairment Loss Recognition

Goodwill Impairment Testing Guide, Examples, & Accounting Tips

Impairment Loss Journal Entry Bronsonarestownsend

Header Q1. (25 Marks) Calculation Of And Journal Entries For Impairment

Ias 36 Pdf

Accounting For Impairment Of Goodwill Ifrs & Aspe (rev 2020) Youtube

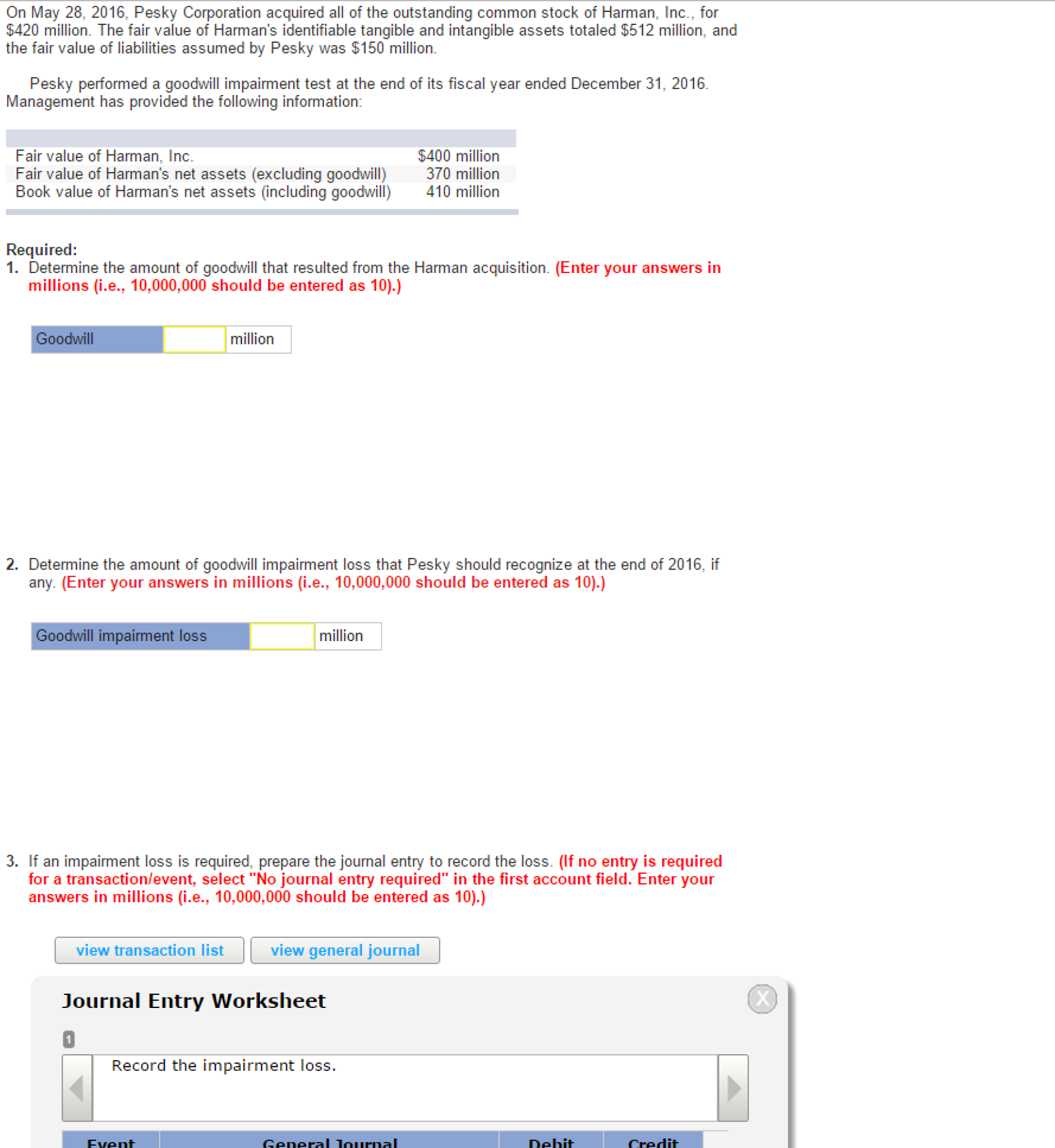

Solved On May 28, 2016, Pesky Corporation Acquired All Of

The New Guidance For Goodwill Impairment Cpa Journal